If you're wondering, "Are mortgage rates going down in Kansas City?" you are entering a…

When is the right time to refinance if rates are slowly declining?

1. Focus on the “Break-Even Point,” Not Just the Rate

Instead of waiting for a specific interest rate, calculate your break-even point. This is the amount of time it takes for your monthly savings to cover the upfront closing costs of the refinance.

- The Calculation: Total Closing Costs ÷ Monthly Savings = Months to Break-Even.

- The 2026 Standard: Many lenders currently prefer to see a break-even point of 36 months or less.

- Decision Rule: If you plan to stay in your home significantly longer than your break-even period, refinancing now can provide immediate financial relief.

2. Use the “1% Rule” as a Guideline, Not a Law

While a traditional rule of thumb is to refinance when rates drop by 1%, in 2026’s higher-cost environment, even a 0.75% to 1.0% drop can be a “game-changer” for your monthly cash flow.

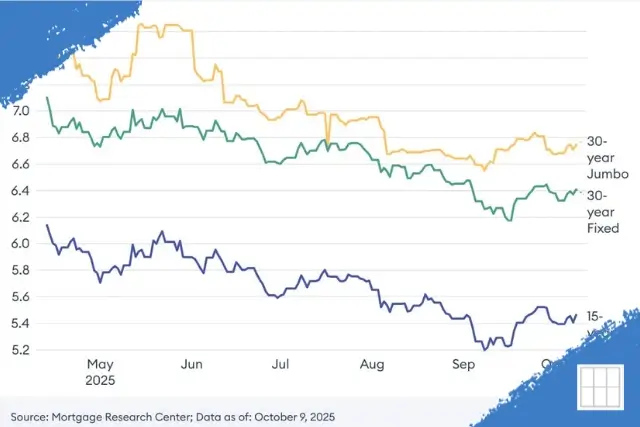

- High-Rate Borrowers: If you locked in a rate above 7% during the peak of 2023–2024, dropping to today’s rates near 6.18% can provide massive savings.

- Small Drops Count: Waiting for an extra 0.25% drop while paying a much higher rate today might cost you more in total interest than you’ll eventually save.

3. Explore Your Refinancing Options

Choosing the right program is just as important as the timing. Depending on your current loan, one of these refinance mortgage options may be right for you:

- Rate-and-Term Refinance: The most common path to lower your monthly payment or shorten your loan term. Learn more in our complete guide to rate-and-term refinancing.

- FHA Streamline: If you have an FHA loan, you may be eligible for an FHA Streamline Refinance, which typically requires no appraisal and minimal paperwork.

- Cash-Out Refinance: Tap into your equity for home improvements or debt consolidation with a cash-out refinance.

4. Consider the “No-Cost” Refinance Strategy

If you are worried about refinancing too soon before rates drop further, a “no-cost” refinance may be an ideal solution.

- How it works: The lender covers the closing costs in exchange for a slightly higher interest rate than the absolute market low.

- The Benefit: Since you didn’t pay thousands in upfront fees, you don’t have a long break-even period to worry about. If rates drop significantly again, you can refinance once more without having “wasted” money on previous closing costs.

5. Take the Next Step with Our Tools

Don’t guess your savings. Use our mortgage refinance calculator to find your specific break-even point today. If you’re ready to see what rates you qualify for, you can get pre-approved online in minutes.

The Bottom Line: “Marry the House, Date the Rate”

In 2026, the strategy is about cash flow today rather than guessing the future. If the current available rate significantly lowers your payment and clears your break-even costs, it is likely the right time to move.

Mortgage rates do not move in lockstep with the Federal Reserve but often mirror the 10-year Treasury yield.

Related Posts