Owning a home outright is a dream for many—a symbol of financial freedom and security…

Can You Afford Your Dream Home in Kansas City? Using an Affordability Calculator

Dreaming of a home in Kansas City, MO, or Kansas City, KS? Our interactive home affordability calculator helps you determine exactly how your dream home aligns with your financial reality. Learn how to navigate the tool and understand how income, personal debts, and distinct local costs—like property taxes—impact your purchasing power across the Kansas City metro.

Why Use an Affordability Calculator in Kansas City?

The Kansas City housing market remains highly attractive, with median home values hovering around $255,000 to $295,000, making it an excellent destination for growing families and first-time buyers. However, localized expenses can heavily shift your actual borrowing limit. Property taxes vary noticeably across state lines (~1.4% in Kansas City, MO vs. ~1.6% in Kansas City, KS), and area homeowners insurance averages roughly $1,200 to $1,500 annually. Utilizing a dedicated affordability calculator accounts for these variables, ensuring you build a realistic house-hunting budget for neighborhoods like Brookside, Waldo, or Overland Park.

How to Use Our Kansas City Affordability Calculator

Our tool maps out an accurate home price range based on your current financial profile and local market data. For the best results, follow these four simple steps:

1. Enter Your Monthly Income

Input your total gross monthly income (your earnings before taxes are deducted). For instance, a household in the Kansas City metro earning a combined $60,000 a year starts with a baseline monthly income of $5,000.

2. List Your Monthly Recurring Debts

Factor in your ongoing obligations, including auto loans, student debt, or minimum credit card payments. Local mortgage lenders prefer a debt-to-income (DTI) ratio below 43%, keeping your specific housing expenses at or under 33% of your income. If you carry $1,000 in monthly non-mortgage debts, a standard DTI framework means roughly $1,650 of a $5,000 monthly income can be comfortably allocated toward your mortgage principal, interest, taxes, and insurance.

3. Choose Your Down Payment Strategy

A larger down payment lowers your principal loan balance and permanently reduces your monthly payment. Kansas City buyers typically leverage a few key programs:

- Conventional Loans: Usually require 5% to 20% down ($12,500 to $50,000 on a $250,000 purchase).

- FHA Loans: Require as little as 3.5% down ($8,750 for a $250,000 home). To run these specific numbers, use our specialized FHA loan calculator.

- VA Loans: Offer 0% down payment options for qualifying military veterans and active service members. Explore your benefits with our VA loan calculator.

- MHDC Programs: The Missouri Housing Development Commission provides competitive down payment assistance grants specifically for buyers on the Missouri side of the metro.

4. Input Current Interest Rates and Loan Terms

With average 30-year fixed mortgage rates pacing between 6.0% and 6.5%, a $200,000 loan balance (assuming a 20% down payment on a $250,000 home) at a 6.25% interest rate creates a baseline monthly principal and interest payment of roughly $1,231. Factoring in $292 per month for Missouri property taxes (1.4%) and an estimated $100 per month for homeowners insurance brings your real-world monthly total to approximately $1,623.

Take Control of Your Budget: Head over to our comprehensive mortgage affordability tool to test different scenarios and find the exact price range that works for you.

What Affects Affordability in Kansas City?

Several regional factors play a heavy role in calculating your total buying power:

- Property Taxes: Jackson County (Kansas City, MO) averages around 1.4% ($3,500/year for a $250,000 home), whereas Wyandotte County (Kansas City, KS) trends higher at approximately 1.6% ($4,000/year for the exact same home price).

- Neighborhood Price Variations: Home values shift quickly across the metro, moving from accessible entry points around $200,000 in Waldo to upward of $350,000+ in master-planned communities like Lee’s Summit or Overland Park.

- Homeowners Insurance Rates: Midwest weather patterns mean budgeting roughly $1,200 to $1,500 annually, with minor premiums increases in storm-prone suburbs like Raytown.

- HOA and Maintenance Fees: Don’t overlook neighborhood-specific HOA fees or standard annual upkeep reserves (ideally budgeting about $2,500/year for a $250,000 property).

Our tools automatically pull these regional figures together to eliminate guesswork. To see an isolated breakdown of your standard monthly obligation, plug your numbers into our primary mortgage calculator.

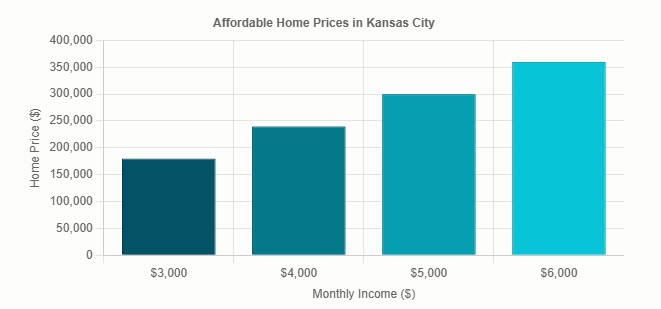

Kansas City Affordability by Income

Curious where you stack up? Here is a general breakdown of home buying power in the Kansas City market based on gross income (calculated using a standard 20% down payment, a 6.25% interest rate, and a 30-year fixed term):

Chart: Affordable home prices in Kansas City based on monthly income, including local taxes and insurance.

To customize this matrix with your exact down payment size and debt profile, access our main affordability calculator.

Tips to Stretch Your Buying Power in the Metro

- Leverage Local First-Time Buyer Programs: Missouri’s MHDC program provides excellent assistance on the MO side, while Kansas Housing Resources Corporation (KHRC) offers matching down payment grants in Kansas City, KS.

- Target High-Value Submarkets: Vibrant communities like Waldo, Grandview, or Raytown regularly offer highly functional single-family homes under the $250,000 mark.

- Optimize Your Credit & Debt Profiles: Eliminating a single credit card balance or a lingering personal loan rapidly lowers your DTI, instantly expanding your maximum loan approval limit.

- Evaluate Refinance Math Down the Road: If you purchase a home now and market rates ease in the future, you can seamlessly recalculate your savings using our mortgage refinance calculator.

Frequently Asked Questions

How much home can I afford in Kansas City with a $5,000 monthly income?

Assuming a standard $1,000 monthly debt profile and a 20% down payment, a $5,000 gross monthly income typically qualifies you for a home priced between $250,000 and $300,000 in Kansas City, MO. Use our affordability calculator to input your exact figures.

Do local property taxes impact my overall pre-approval amount?

Absolutely. Because property taxes are bundled into your monthly escrow payment, higher rates (like Wyandotte County’s ~1.6% average) add roughly $333 a month to a $250,000 home purchase, which reduces the total loan amount a lender can approve compared to lower-tax areas.

Are there down payment assistance options for Kansas City buyers?

Yes. Buyers on the Missouri side can apply for MHDC down payment grants, while Kansas buyers can utilize KHRC initiatives. Additionally, FHA loans across the entire metro require just 3.5% down, and VA loans offer 0% down for eligible military families.

More Kansas City Homebuying Resources

Explore our suite of specialized digital tools designed to make your home purchase straightforward and stress-free:

- Affordability Calculator – Establish a bulletproof home buying budget.

- Mortgage Calculator – Estimate your principal, interest, taxes, and insurance payments.

- How to Budget for a Home in Kansas City – Our comprehensive regional financial guide.

- First-Time Homebuyer Programs in Kansas City – A full breakdown of local grant opportunities.

- View All Mortgage Guides – Access our complete mortgage education library.

Related Posts